Methodology

Health and wealth consumer index score

A survey of more than 2,000 randomly selected U.S. adults was conducted in the fall of 2023 to gauge physical, financial and mental health across the country. The survey was commissioned by HSA Bank and executed by a third-party organization.

This year, respondents have been scored based on their responses to 18 questions about their health plan enrollment status, health practices, mental health, ability to pay for health-related expenses and confidence in their own health and wealth. Each survey respondent receives a health score and a wealth score, which are combined to produce their overall health and wealth consumer index score.

The health and wealth consumer index score for each respondent ranges from zero to 100. The maximum score is 50 for health and mental health combined, and 50 for wealth. The higher the score, the better the respondent ranks in terms of their physical, mental and financial health engagement.

Respondents are grouped into four categories based on their health and wealth consumer index score:

![]()

Minimally engaged (Score range: 0-39): Rarely prepare for healthcare expenses and do not take an active role in managing their health

![]()

Moderately engaged (Score range: 40-59): Participate in roughly half of health and wealth activities that contribute to engagement

![]()

Highly engaged (Score range: 60-74): Participate in most of the behaviors that contribute to health and wealth engagement

![]()

Optimally engaged (Score range: 75-100): Take active steps to maintain or improve their health and health-related finances

The margin of error for this sample size is +/- 2.18% at the 95% confidence level. Smaller subgroups have larger margins of error.

Insights & action

Insights & action

Employers can share the Health & Wealth Index Calculator as an index supplement to further engage employees in their health and wealth. The results can help employees balance decisions and expenses during their working years and ultimately throughout retirement.

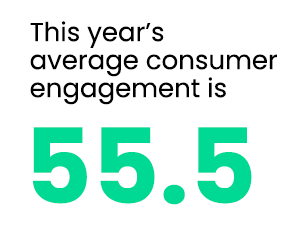

2024 consumer engagement scores

Overall, this year’s average index score of 55.5 is slightly down from 56.6 in 2023, yet remains well within the “moderately engaged” category. Even with the minor decline, this score indicates continued positive levels of health and wealth engagement among Americans.

With so much to focus on, it can be challenging to capture someone’s attention. Let alone hold it. So how do employers get employees to engage in their benefits offerings? Education. And with benefits relevant to their employees’ lifestyles.

The annual HSA Bank Health & Wealth Index provides insight into health and wealth engagement of consumers across the country. And employers can use this information to tailor health and wellness benefits to the needs of their employees. Employers can offer alternate savings methods through varied accounts, while meeting employees where they are with incentive-based programs. These solutions are best combined with thorough education on which account best fits their needs, how they can spend and save wisely, and how they can use these accounts to prepare for the future.

Generational gaps in health plan cost awareness

To no surprise, cost remains the primary reason why someone is not currently enrolled in a health plan. Of those surveyed who are not currently enrolled in a health plan, 53% said it was due to cost, an increase from the 51% reported last year.

Generational differences are clear, too. Those in Generation Z continued to be less familiar with their health plan’s costs. They’re followed by millennials, those in Generation X and then baby boomers.

Confidence to cover healthcare costs remains somewhat consistent over the past three years (66%). Yet, 36% of those surveyed are not sure how to pay for healthcare expenses in retirement, and 35% are not even sure how to cover healthcare costs in the next year.

When asked to report on their confidence in a series of questions about healthcare costs, baby boomers responded with high confidence percentages across the board. As did college graduates and those earning over $100,000 annually.

Overall, respondents reported their level of confidence to:

Insights & action

Insights & action

With healthcare cost and plan understanding of such great concerns, it’s beneficial to educate employees that a better understanding can yield cost savings. HSA Bank offers Health Savings Accounts (HSAs) that help employees save and pay for healthcare expenses, but also offers tools to guide them in choosing the right health plan for their unique needs.

The importance of health plan coverage and attaining preventive services

There is no argument against the importance of preventive healthcare. But sometimes health plan coverage could mean the difference between accessing care and letting healthcare lapse if it means paying out of pocket.

When asked to report to what extent they agree or disagree in whether their current health plan helps them attain necessary healthcare while managing costs, those with HSA-eligible health plans and Health Reimbursement Arrangements (HRAs) scored higher when compared with other health plans.

This may indicate that the ability to save on healthcare expenses engaged respondents to seek and attain healthcare.

When asked what is most important when choosing a healthcare provider or service, Network ranked highest at 25%. There was also an increase last year in Quality and Expertise/Specialty from 21% to 23% and 13% to 15% respectively.

Overall, respondents reported that they visited their doctors and providers more than ever. Visits to primary care physicians or specialists increased to 89% — the highest response rate since 2020.

And since 2020, when it saw a large increase, telehealth remains a popular option, with half of respondents reporting that they utilized this service in the last year. Negatively, preventive screenings are down with each category showing a lower response rate from the previous year.

Baby boomers and Gen Xers engaged more in preventive healthcare, with the exception of online health assessments and biometric screenings (millennials and Gen Zers are more engaged with wellness program initiatives). Just 7% of total respondents reported having had a biometric screening in 2023, with 10% of respondents having obtained none of the preventive healthcare listed above.

Insights & action

Since more respondents with HSA-eligible health plans and HRAs reported that they attained healthcare while managing costs, it could be beneficial for companies to offer these health accounts. Active participation, such as attaining preventive healthcare, is a hidden benefit. Employers can promote these accounts, emphasizing the importance of preventive care.

Generational differences in lifestyle changes made

With respondents reporting fewer preventive healthcare visits than last year, it may be even more important for employers to offer incentives to employees making positive lifestyle changes.

Millennials and Gen Zers, college graduates and those earning over $100,000 annually are more willing to make lifestyle changes demonstrating that these respondents are active participants in their healthcare management.

Regarding what lifestyle changes were implemented, improving eating habits had the highest response rate at 66%, followed by increasing physical activity at 58%, managing stress at 42%, and improving mental health at 36%.

Baby boomers focused more on improving eating habits and increasing physical activity whereas younger respondents like Gen Zers and millennials (both 47%) reported twice as high as baby boomers (23%) to improving mental health.

Focus on improving mental health:

Insights & action

A Lifestyle Spending Account (LSA) offered by employers can help employees save on items like gym memberships, mental healthcare and more to improve their well-being.

The impact of work and financial stress on mental health

The rise in mental health awareness is nothing short of necessary. And with younger generations like Gen Zers and millennials actively trying to improve their mental health, employers should take notice.

Workplace stress is real and is affecting most working generations. Nearly one-third Gen Zers, 29% of millennials, and 21% of Gen Xers reported feeling stressed at work.

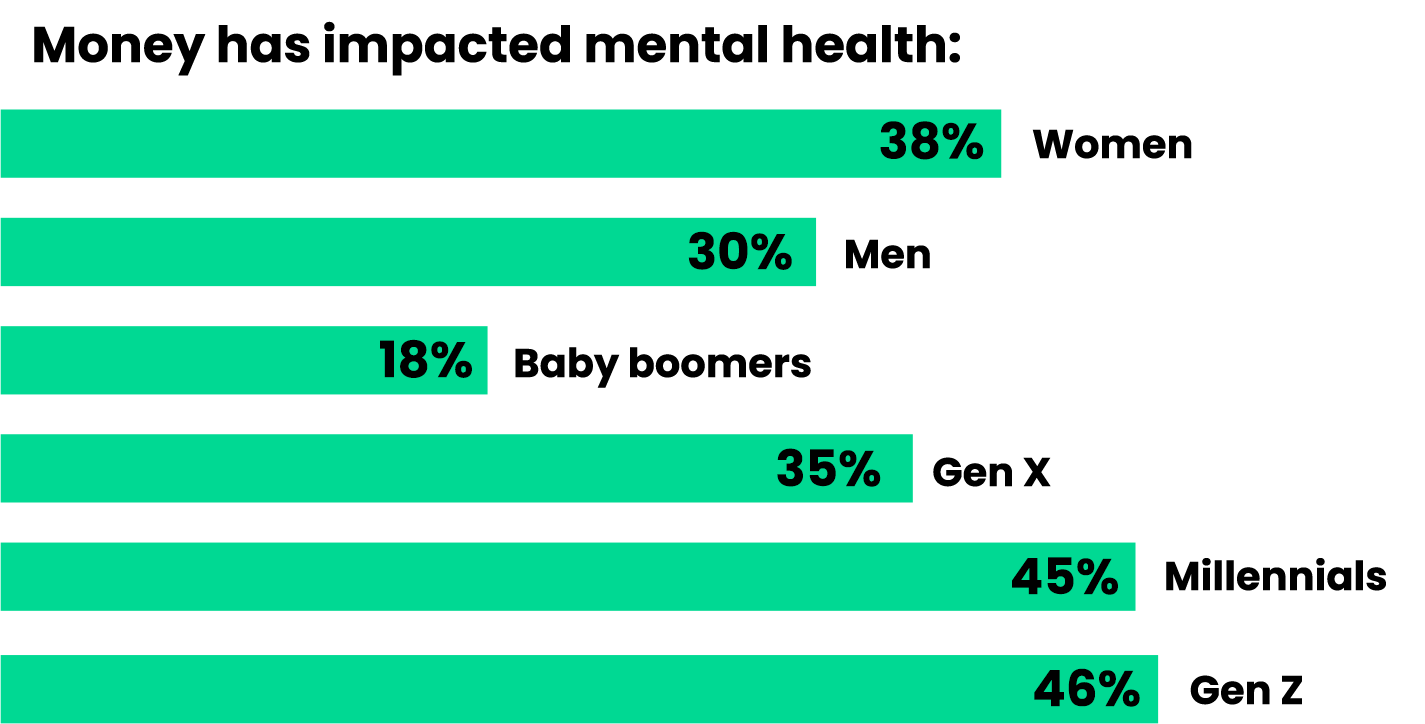

And money is having an impact on their mental health, affecting nearly half of younger generations (46% of Gen Zers and 45% of millennials) surveyed.

Baby boomers reported far less stress at work (5%) and money impacting their mental health less (18%), most likely due to more earning and savings years behind them.

When respondents were asked about mental health specifically, baby boomers reported placing equal value (18%) on health-related concerns and money impacting them.

Women struggle more with mental health compared to men when it comes to money impacting their mental health, regretting financial decisions, limiting social media due to a negative impact on mental health, work stress and health-related concerns negatively impacting how they feel.

Insights & action

A greater focus on mental healthcare is just the beginning. Accessibility is a start, but coverage and money-saving options are a greater help employers can provide. Related support like therapy, psychiatric care and prescription drugs are IRS-eligible expenses under HSAs, FSAs and HRAs. LSAs and Emergency Savings Accounts (ESAs), for instance, help make paying for mental healthcare less of a financial stressor. And employer-sponsored Adoption Assistance can help decrease the stress employees may face during the adoption process.

Money-saving accounts and employer benefits contribute to wealth

Savings. It’s not just what respondents put away for unexpected expenses or retirement but also cost savings that contributes to wealth.

New for this report, we asked respondents if they made changes to improve wealth and finances in the past year. Sixty-nine percent of respondents replied yes. Of those, 45% created a budget, 41% paid off debt, 33% invested their savings, and 27% specifically saved for an emergency.

While men and women respondents reported equal engagement in HSA contributions, HSA spending and account monitoring/management of their HSAs, men more than women leaned more toward investment and saving for future healthcare expenses. Additionally, women reported carrying the burden of worry about current or future medical bills.

Who invests their HSA dollars?

Breaking down the information further, women reported being more likely to create a budget or pay off loans, but less likely to invest savings or fund their retirement account.

High-income respondents reported being more likely to pay off debt, invest savings and fund their retirement account, but less likely to create a budget.

Baby boomers reported being most likely to have paid off debt. And Gen Zers and millennials dominated the budget, emergency savings and invested savings categories.

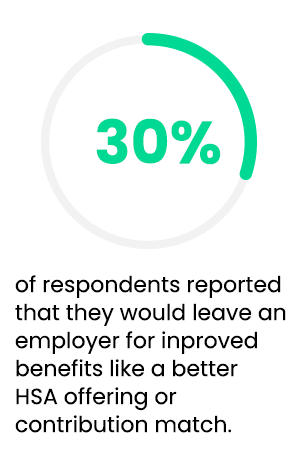

Furthermore, 30% of respondents reported that they would leave an employer for improved benefits like a better HSA offering or contribution match.

They’re also aware that healthcare costs will most likely rise in the next year. Based on this, 28% of respondents reported that they would consider putting off medical care until it becomes affordable, and 26% reported that they would tap into their emergency fund or retirement fund to curb costs. In fact, across all income ranges, respondents reported that they are more likely to do this than increase their HSA contributions. Yet, for those with access to an HSA, it’s one of the best ways to save for healthcare expenses since funds are completely tax free when used for IRS-qualified expenses.

Insights & action

Given this perspective, an HSA paired with employer contributions is a powerful combination. Employer contributions to HSAs could not only help companies retain employees but also give employees peace of mind knowing they may not have to attain additional employment or put off healthcare visits. An additional benefit of an HSA is the ability to invest the funds, so employees’ savings could potentially grow even more. And, adding an employer-sponsored Emergency Savings Account (ESA) to a benefits offering could further help employees when the unexpected occurs. This differs from an HSA in that the money saved can be used for anything without penalty.

Each year, HSA Bank gathers and analyzes data so we can better understand the behaviors, habits and education level of healthcare consumers. We identify and track trends in an effort to provide a more robust account offering and experience. Our goal is to help our members make the most of their accounts — through both saving and spending – because we understand the importance of health and wealth. Our resources are specifically developed to thoroughly educate while they inspire continuous engagement and confidence.